Introduction

The recent decision by a federal judge to reverse a rule concerning medical debt on credit reports has sent ripples through the financial community and beyond. The implications of this ruling are profound, affecting countless individuals burdened by medical debt. This blog post explores the details surrounding the federal judge’s decision along with the legal and financial landscape that shapes the ongoing discourse on medical debt and credit reporting.

Understanding the Ruling

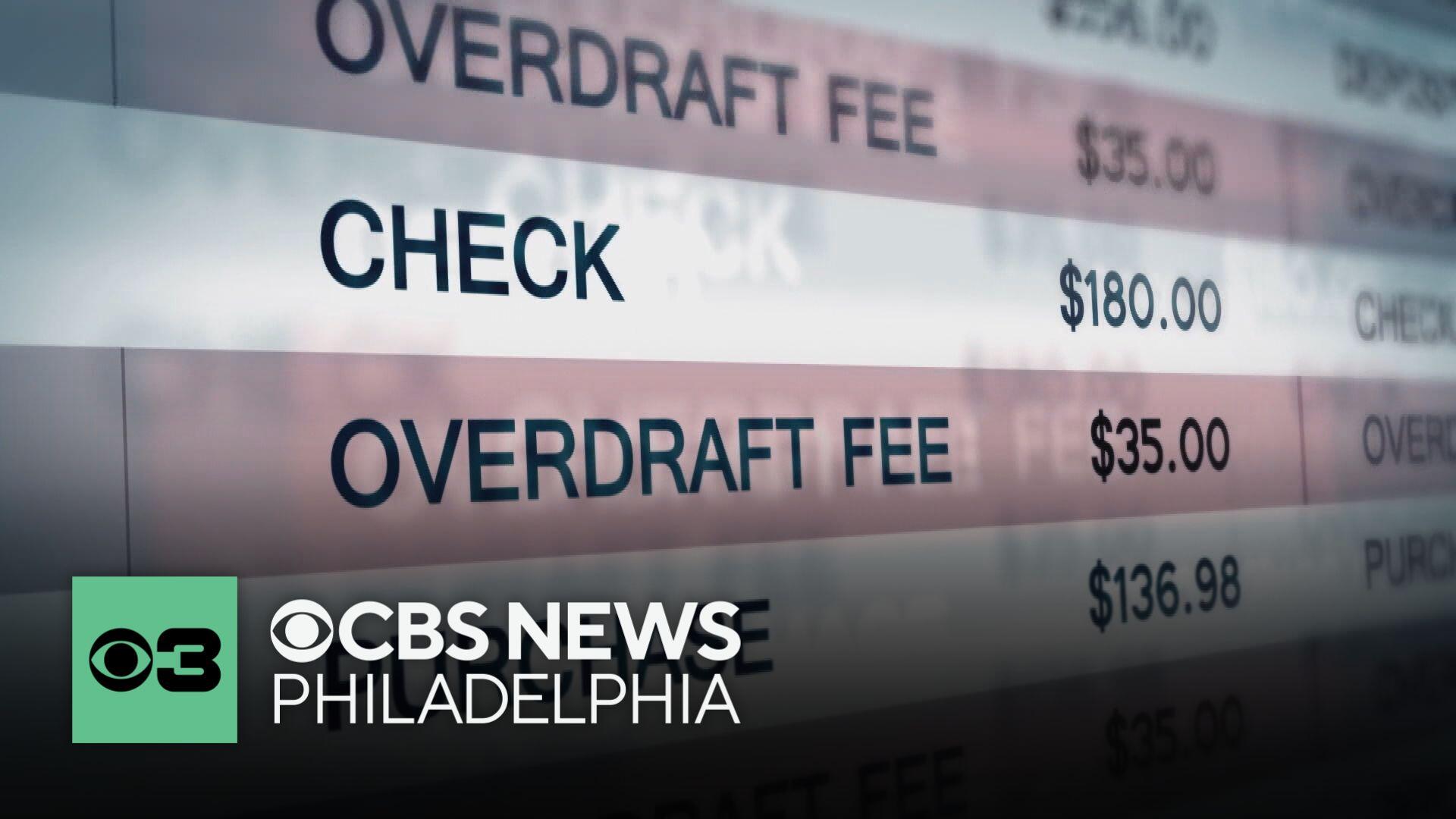

According to a report by CBS News, the judge’s ruling effectively negates the Consumer Financial Protection Bureau’s (CFPB) efforts to create more favorable conditions for consumers grappling with medical debts. These debts often lead to detrimental credit reports, creating barriers to employment, housing, and more.

This ruling has thrown into question the future of how medical debts will be treated in relation to credit reporting. The previous regulation, supported by the CFPB, aimed to provide consumers with additional protections and aimed to limit the damage such debts could inflict on credit scores. However, with the reversal now in place, the earlier arrangements are no longer enforceable.

The Impact of Medical Debt on Consumers

Medical debt affects millions of Americans, significantly impacting their financial health and access to essential services. It often ranks as the leading cause of personal bankruptcy in the United States. This new ruling means that medical debt could now immediately affect a consumer’s credit report shortly after being incurred, rather than after a grace period that the CFPB rule would have provided.

For many Americans, unexpected medical expenses can result in overwhelming financial hardship. Individuals who are uninsured or underinsured face steeper challenges. This reversal can lead to a domino effect where an individual’s creditworthiness is unnecessarily tarnished, complicating their ability to secure loans or even rent an apartment.

Analyzing the Legal Landscape

The legal landscape regarding medical debt is complex. The CFPB’s initial goal was to raise awareness about the impact of medical debt on credit scores and to shift the narrative towards seeing medical debt as different from other types of debt, largely due to its often unavoidable nature.

The reversal by the federal judge raises significant concerns about consumer protections and the accountability of financial institutions. Advocates for consumers argue that the decision may benefit creditors at the expense of individuals trying to navigate their financial responsibilities.

This incident serves as a stark reminder of the gaps in consumer protection in the current economic climate. The ruling may prompt calls for legislative changes aimed at protecting consumers from the hardships associated with medical debt.

What Businesses and HR Professionals Need to Know

For HR professionals and business leaders, understanding the repercussions of this ruling is essential. Employees’ financial wellbeing directly correlates with productivity, morale, and workplace stability. With the possibility of increased medical debt impacting employees’ financial health and credit scores, organizations should be proactive in supporting their workforce.

Implementing programs focused on financial literacy can empower employees to make informed decisions about medical debt and other financial issues they may face. Additionally, organizations may want to consider providing support services that help employees navigate expenses related to healthcare more effectively.

Emerging Solutions and Workflows

As we delve deeper into the complexities of medical debt, it’s crucial for businesses to utilize modern solutions that can help automate their processes. By leveraging AI and n8n workflows, companies can streamline their operations, enabling efficiency and better resource allocation in addressing employee concerns over medical debt.

For example, companies can automate communication regarding benefits and healthcare options, making it easier for employees to understand what support is available to them. By integrating automated tools that facilitate access to financial resources and advice, organizations can better assist employees in managing the challenges posed by medical debt.

Conclusion

The recent ruling by a federal judge to reverse the medical debt rule has created a significant shift in the way financial institutions and consumers will navigate medical expenses in relation to credit reporting. The implications of this decision extend beyond individual consumers; they touch upon the very fabric of workplace dynamics and employee welfare.

As we watch this story unfold, it is essential for organizations to stay informed and adapt their policies and support mechanisms accordingly. Empowering employees with the knowledge and resources they need to handle medical debt can not only improve individual outcomes but also enhance overall workplace health and productivity.

In an age where financial stability is increasingly at risk, proactive measures in the workplace can lead to a more resilient workforce prepared to face challenges head-on. The journey towards equitable solutions for medical debt continues, and staying ahead of such developments is imperative for all stakeholders involved.